You’ve bought crypto. You’ve sold crypto. And at some point, you’ve probably had a bank transfer delayed, flagged, or outright blocked, with little explanation from your bank. It’s one of the most frustrating realities of the crypto space, and it hasn’t gone away entirely, even as the industry matures.

The good news is that the landscape has shifted significantly in 2026. Regulatory clarity is improving, traditional banks are warming up, and a growing list of digital-first institutions is actively competing for crypto users’ business. The bad news is that “crypto-friendly” still means very different things depending on the institution and picking the wrong bank can cost you time, money, and access to your own funds.

This guide cuts through the marketing and tells you what’s actually changed, what to look for, and which crypto friendly banks are genuinely worth your time in 2026.

Best Crypto-Friendly Banks for Retail Users

1. Revolut

Revolut is the closest thing to a full crypto banking experience for retail users in 2026. The UK-based fintech offers cryptocurrency trading right within its mobile app, with support for over 30 cryptocurrencies, including Bitcoin and Ethereum. Users can exchange between different fiat and digital currencies, set up cryptocurrency vaults to save and accumulate digital assets over time, and manage crypto alongside traditional money in a single account.

Available across the EU, UK, US, and a growing number of international markets, Revolut is the go-to option for retail users who want convenience above all. The tradeoff is that Revolut is not a bank in the traditional sense in all jurisdictions — check whether local deposit protection schemes in your region cover your deposits.

Best for: Everyday crypto users who want to buy, sell, and hold within a single app.

2. Ally Bank

Ally Bank has maintained its crypto-friendly stance since 2017, offering Coinbase integration and treating crypto transfers as legitimate financial activity without delays or blocks. While Ally doesn’t offer direct crypto trading within the app, it lets you link your account to external exchanges and funds without the friction that plagues many traditional banks.

You can also invest through Ally Bank in funds that own crypto, such as Grayscale Bitcoin Trust (GBTC), or those that own crypto futures like ProShares Bitcoin Strategy ETF, giving indirect crypto exposure through regulated investment vehicles.

Best for: US-based retail investors who want a reliable, FDIC-insured bank that won’t interfere with their crypto activity.

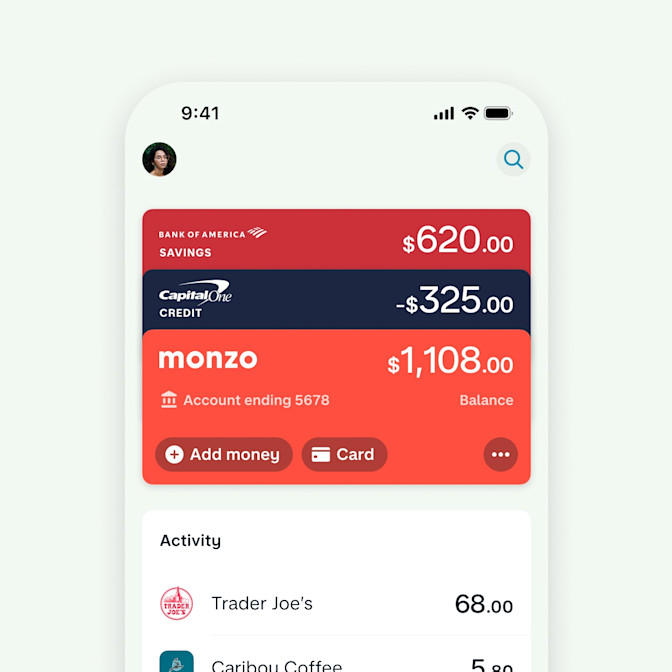

3. Monzo (UK)

Monzo is the UK’s strongest option for bringing cryptocurrency into mainstream banking in 2026, offering FCA-regulated exchange remittances, crypto tracking via the app, multi-currency budgeting, and real-time fraud detection alerts. Monzo’s strict compliance history has given it a stable, trusted reputation in the UK market, and its app experience is among the best available.

Best for: UK-based retail users who prioritise security, a polished user experience, and FCA-regulated compliance.

4. Cash App

Cash App allows US users to buy, sell, and hold Bitcoin directly within the app, with options to withdraw to a personal wallet — one of the few mainstream consumer apps that supports on-chain Bitcoin withdrawals. It’s simple, widely available, and doesn’t require opening a separate exchange account to get started.

Best for: Beginners in the US who want the simplest possible entry point into Bitcoin, without multiple accounts.

Best Crypto-Friendly Banks for Businesses and Startups

5. Mercury

Mercury serves thousands of crypto startups, including Phantom and Rarible. It offers purpose-built infrastructure for Web3 businesses, with the critical feature of displaying business names on wire transfers — important for compliance and counterparty trust. Mercury doesn’t allow you to hold cryptocurrency directly, but there are no restrictions on crypto-related business activity.

Mercury’s Vault product extends FDIC insurance coverage to up to $5 million, and its Treasury product provides an attractive yield on balances over $500,000 — making it a practical option for crypto businesses that need to manage significant fiat reserves alongside their digital asset operations.

Best for: Web3 startups and crypto-native businesses that need reliable USD banking without crypto interference.

6. Custodia Bank

Custodia Bank, formerly Avanti, is a Wyoming-chartered Special Purpose Depository Institution (SPDI) designed specifically to bridge blockchain finance and the US banking system. It operates on a 100% reserve model, providing institutional cash management and Bitcoin custody for digital asset companies. For crypto businesses that need a US bank with actual Bitcoin custody capability under a regulated framework, Custodia is one of very few options.

Best for: US-based crypto businesses and institutions that need regulated Bitcoin custody alongside traditional banking services.

7. Wirex

Wirex supports a multi-currency wallet covering over 30 fiat and digital currencies, offers a crypto debit card that auto-converts crypto to fiat at checkout, and provides cashback in WXT tokens. It is FCA-licensed and compliant with AML rules, with global reach across the EU, UK, and APAC regions. For businesses operating across multiple currencies and markets, Wirex’s infrastructure removes a lot of the friction that comes with traditional multi-currency banking.

Best for: Internationally focused businesses that need seamless fiat-crypto conversion and multi-currency support.

8. Brex

Brex functions as a finance platform with spend controls, treasury features, and stablecoin functionality, best suited for internal finance operations rather than core settlement infrastructure. It works well alongside a primary banking relationship for managing internal spend and stablecoin-based treasury operations but should not be used as a standalone banking solution for crypto businesses.

Best for: Funded startups needing stablecoin-compatible spend management alongside a primary banking setup.

What Does “Crypto-Friendly” Actually Mean?

The term gets used loosely, so it’s worth being precise. A truly crypto-friendly bank does at least three things reliably:

1. It doesn’t block or flag transfers to and from legitimate crypto exchanges. This sounds basic, but many banks still treat transfers to Coinbase, Binance, or Kraken as suspicious activity and will delay, review, or freeze them without warning.

2. It doesn’t close your account because of crypto activity. Account closures tied to crypto use, even fully legal, documented activity have become less common in 2026 but are not gone. A genuinely crypto-friendly bank has clear, written policies on what crypto-related activity is permitted.

3. It offers at least one active crypto feature or integration. This could be the ability to buy and sell crypto within the app, links to major exchange accounts, crypto-backed loans, or custody services. Banks that merely “tolerate” crypto transfers without offering anything proactive are better described as crypto-neutral, not crypto-friendly.

A lot of banks like to market “Web3 support” or “blockchain strategy” while quietly flagging every transfer to an exchange. That is window dressing, not support.

Why Do Banks Block Crypto Transactions?

Before choosing a bank, it helps to understand why so many institutions are still cautious and why even good banks sometimes block legitimate transactions.

Banks freeze crypto transfers when automated compliance systems cannot clearly identify the transaction’s source, purpose, or structure within regulatory expectations. Most crypto-related bank freezes are structural rather than punitive triggered when a transaction cannot be clearly categorized or explained within standard banking logic.

In practice, this means the problem is often not the bank’s policy on paper, but the automated risk-scoring system running in the background. These systems look at transaction patterns, counterparties, jurisdictions, and payment rails. When your transfer to a crypto exchange doesn’t match what the system expects from a “normal” banking customer, it gets flagged regardless of whether you’ve done anything wrong.

Banks have become far more cautious about transfers involving cryptocurrency platforms. Many institutions treat these transactions as high-risk because of the volume of fraud tied to crypto investment scams. Instead of allowing instant debit-card transfers, banks may force the transaction through a slower ACH process, adding several days of delay.

There’s also a capital penalty at play in some markets: new EU regulations impose a 1,250% risk weight on unbacked crypto assets such as Bitcoin and Ethereum; a capital penalty that makes crypto exposure commercially unviable for traditional institutions, regardless of the actual risk individual clients present.

What to Look For in a Crypto-Friendly Bank

Before we get to specific recommendations, here’s a framework for evaluating any bank you’re considering:

Clear written policy on crypto transactions. Don’t rely on what a customer service agent tells you. Find the bank’s actual policy documentation. If it doesn’t exist or is vague, that’s a red flag.

Support for your preferred exchanges. Some banks allow transfers to Coinbase but block Binance. Others restrict withdrawals from decentralised exchanges. Know which platforms you use and verify compatibility.

Transaction limits that work for you. Some crypto-tolerant banks impose daily or monthly limits on exchange transfers. These may be fine for retail investors making occasional trades but unworkable for active traders or businesses.

Fiat currency support. If you’re trading globally, you need a bank that handles multiple currencies efficiently or at least processes USD, EUR, and GBP transfers without excessive fees.

FDIC or equivalent insurance. Your fiat deposits should be insured. Any crypto balances held directly with a bank or fintech may not be verified before depositing.

Stability and track record. Never rely on a single bank. Maintain accounts at two or three institutions for continuous access. The Juno collapse showed that even popular platforms can fail suddenly.

What About Traditional Big Banks?

The answer here is nuanced and evolving fast. A few years ago, the answer was simple: avoid them for anything crypto-related. In 2026, that’s no longer uniformly true.

JPMorgan, as noted, has reversed its restrictive stance for retail users in the US. Wells Fargo has launched Bitcoin-backed loans for institutional and high-net-worth clients. Bank of America has published supportive crypto research for the first time. These are meaningful signals that the largest US institutions are repositioning.

That said, even legitimate, documented crypto usage can still cause extra scrutiny, lengthy reviews, and account freezes at major banks. The issue became especially acute after the collapse of crypto-friendly banks such as Silvergate, Signature, and Moonstone. Institutions that once served as key bridges between fiat and digital assets, whose exit left a gap few traditional players have been willing to fill.

For retail users, the major banks are now generally usable for basic crypto exchange transfers. For crypto businesses, the picture remains trickier, expect enhanced due diligence, restrictive terms, and the possibility of sudden policy changes.

A Note for African and Global Crypto Users

Most crypto-friendly bank guides are written almost entirely for US and European audiences. If you’re based in Africa, Southeast Asia, Latin America, or other emerging markets, the options look different — and the need is often more acute.

In many African markets, crypto has become a practical tool for dollar access, cross-border payments, and protection against currency devaluation. The gap in traditional banking infrastructure has made crypto adoption faster in these regions than almost anywhere else. But it’s also meant that banking friction, blocked transactions, exchange restrictions, and limited fiat ramps; hits harder.

For users in these markets, the most practical options in 2026 are typically: Revolut where available, local crypto-native fintechs that offer integrated fiat-crypto accounts, peer-to-peer exchanges as a fiat on-ramp alternative when bank transfers are blocked, and global neobanks with regional expansion (Wirex, for example, has been growing its APAC presence). Always verify the regulatory status of any platform in your specific jurisdiction what’s permitted in Nigeria, Kenya, or South Africa differs significantly, and those rules are changing rapidly.

How to Avoid Getting Your Account Frozen

Even with the right bank, smart habits reduce your risk of disruption:

Use bank transfers instead of debit card purchases when possible. Sending crypto to an exchange and then transferring funds into your own bank account has become the highest-risk pattern. ACH and bank wire transfers are treated more consistently than card transactions and are less likely to trigger automated fraud flags.

Keep transaction descriptions clear. When transferring to or from an exchange, ensure the reference clearly identifies the transaction. Vague or missing references are more likely to trigger compliance reviews.

Don’t make multiple small transfers in rapid succession. Structuring-like patterns — even unintentional ones — raise flags. One clean, properly documented transfer is better than five smaller ones.

Inform your bank proactively for large transfers. If you’re moving a significant amount from an exchange to your bank account, a quick call to your bank ahead of time can prevent a freeze. Have your exchange account details and proof of transaction history ready.

Maintain accounts at multiple institutions. If one account is frozen or restricted, having a backup ensures you don’t lose access to your funds at a critical moment.

Frequently Asked Questions

Which bank is the most crypto-friendly overall?

For retail users, Revolut is the most integrated option globally in 2026. For US retail users specifically, Ally Bank offers the most reliable experience at a traditional bank level. For businesses, Mercury leads for Web3-native companies, while Custodia is the strongest option for those needing regulated Bitcoin custody.

Can my bank close my account for using crypto?

It happens less frequently in 2026 than it did previously, but it is still possible — particularly with traditional banks in markets where crypto activity is seen as high-risk. To minimise this risk, use a bank with an explicit crypto-friendly policy, keep transaction documentation, and don’t mix high-volume exchange activity with a personal current account.

Do I need a separate bank account for crypto?

Not necessarily, but many active crypto users find it useful to maintain a dedicated account for exchange-related transfers. It simplifies tax reporting, keeps transaction histories clean, and reduces the risk of your primary account being flagged.

Are crypto bank balances FDIC insured?

Your fiat deposits at an FDIC-member bank are insured up to $250,000 per depositor. Any crypto assets you hold — whether on an exchange, in a bank’s custody product, or in a self-custody wallet — are generally not covered by FDIC insurance. Always verify the specific coverage terms before depositing.

What’s the safest way to move large amounts from crypto to my bank?

Use a regulated, well-established exchange to convert to fiat first. Then transfer via bank wire or ACH rather than debit card. Have documentation of the source of funds ready, and consider notifying your bank in advance for amounts that may seem unusual relative to your normal activity.

The Bottom Line

The relationship between banks and crypto has shifted more in the last 12 months than in the previous five years combined. Regulatory clarity, institutional adoption, and competitive pressure from digital-first banks have forced the industry to move, and for crypto users, that’s broadly good news.

But “crypto-friendly” still requires scrutiny. Your best move in 2026 is not to chase a mythical perfect bank; it is to assemble a resilient stack: one stable home bank in your main jurisdiction that doesn’t panic at the word “crypto,” one specialised digital asset bank or platform for custody, tokenisation, or yield, and one or more well-chosen DeFi and self-custody tools for flexibility.

Pick based on your actual needs, verify policies directly with the institution, and never depend on a single banking relationship for your crypto activity.